Grab: The Super-App Turned Profitable. The Bank Inside It Breaks Even Next — That's the Entry I'm Watching.

A profitable Southeast Asian super app with a credit engine about to cross breakeven and about a third of its market cap in net cash. The inflection that matters here it's GrabFin breakeven in H2'26.

Grab Already Turned Profitable — the Inflection I’d Buy Is Still Ahead

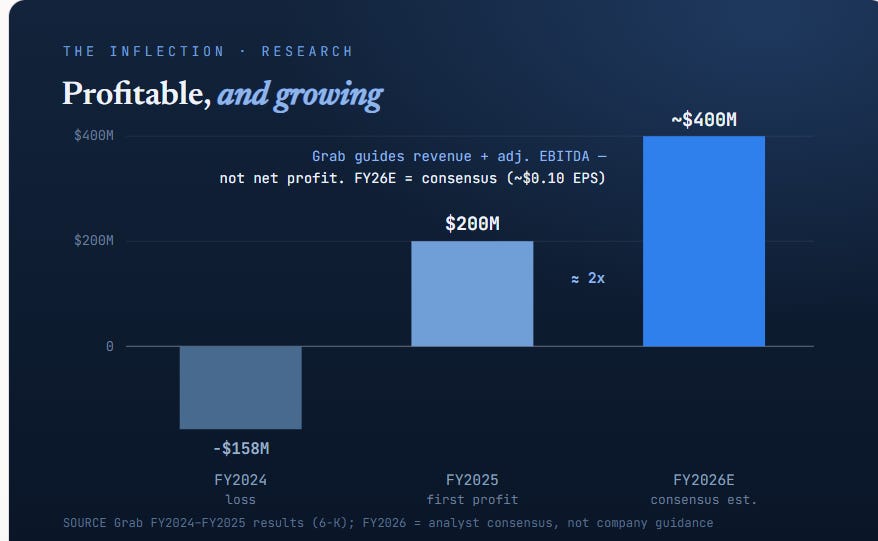

The Inflection is about one thing: businesses crossing into profitability, or great businesses on sale in a dip, before the market re-rates them. Grab booked its first full-year net profit in FY2025, close to $200M, last year was about a "path to profitability" story. Analyst consensus has net profit close to doubling this year FY2026 toward ~$400M, helped by the net interest income Grab now earns on its ~$7B cash pile.

Chart 1 · GRAB profitability inflection. Source: Grab FY2024–FY2025 results & three-year outlook (Q4'25 call); figures adjusted (non-GAAP).

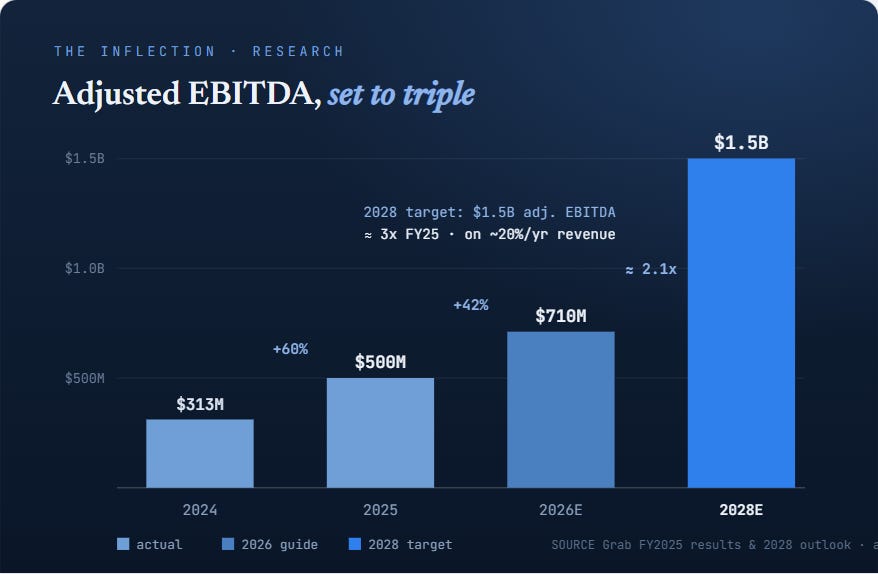

Additionally, Grab's adjusted EBITDA is guided to roughly triple, from $500M in 2025 to $1.5B by 2028, on revenue growing about 20% a year. The first step, the profitability inflection, is done. The next step, cash flow scaling on a business still growing 20%+ is the reason Grab is on my watchlist.

Chart 2. Adjusted EBITDA is guided to 3X by 2028. From $500M in FY2025 to $1.5B 2028 target (≈2.1x the 2026 guide). Source: Grab FY2024–FY2025 results & three-year outlook (Q4'25 call).

Grab at ~$3.90 the stock is about 41% off its 52-week high — which makes this a third, still-attractive angle on Grab: a newly profitable platform whose segment level and cash inflections are still ahead of it.

The question this post works through isn’t “is Grab good”, it’s whether a profitable, cheap, cash-rich super-app whose next inflection is a segment crossing breakeven is enough to start a position, when the cleanest entry already passed.

Cross-sell only matters if the profitable business can fund the unprofitable one — the Ride Business Pays for the Bank

Grab runs three core businesses:

Mobility. ride-hailing.

Deliveries. GrabFood, GrabMart, GrabExpress.

Financial Services. GrabFin — payments, lending, BNPL, and digital banks across the South East Asia.

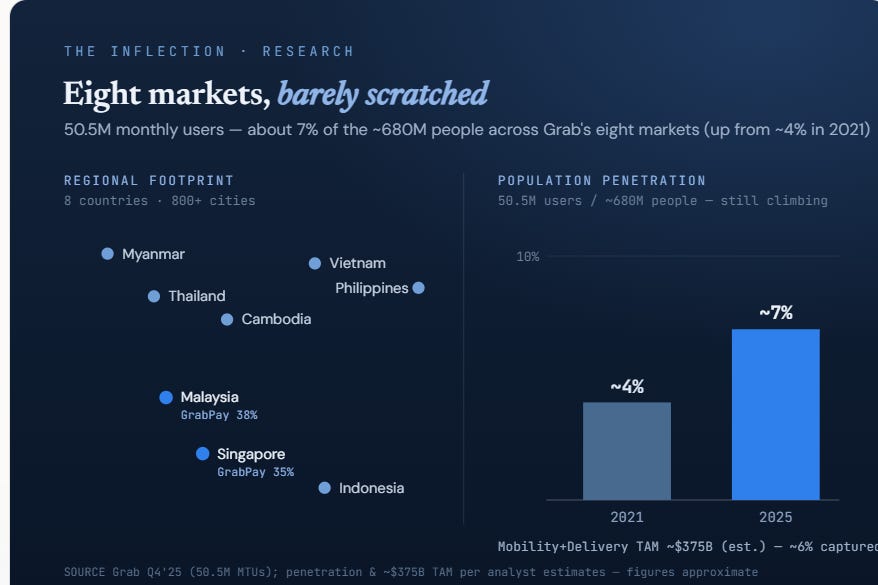

One app, 50.5 million monthly transacting users, about $131 of GMV per user per quarter and a market it has barely begun to penetrate.

Grab operates in eight countries and 800+ cities, yet it reaches only about 7% of the ~680 million people who live in them, up from around 4% in 2021. On a dollar basis it's earlier still: the Mobility-and-Deliveries market it plays in is estimated near $375 billion, and Grab has captured only about 4% of it. Single digit adoption while already profitable, that is a signal most of the growth is still ahead.

Chart 3. Grab’s population penetration. Grab serves ~7% of the ~680M people in its eight markets and about 4% of an estimated ~$375B Mobility and Deliveries TAM.

The engine that widens that penetration is a cross-sell flywheel. A rider becomes a food customer who becomes a GrabPay user who becomes a borrower who becomes a depositor — and the transaction data from all of it makes GrabFin's underwriting sharper, which lowers credit losses, which funds cheaper products, which pulls in more users. That is the exact engine I look for, and the exact engine NU, SoFi and Robinhood run: acquire a user cheaply through one product, then monetize them through payments, lending and take-rate. Same engine, different products, different geography.

The moat has two strenghts:

First, logistics density: more orders in a city means shorter routes and lower cost to serve — a supply-side advantage a new entrant can't replicate quickly.

The second is embedded distribution in fintech: GrabFin's digital banks hold 7.4 million depositors, and the company says nearly all were converted from the existing user base rather than bought with marketing, a near-zero acquisition cost on a deposit franchise.

The risk is the on-demand business competition (ShopeeFood, GoTo). Grab's real rivals in Southeast Asia are GoTo and Sea Limited. GoTo is the structurally comparable one: the same three businesses in the same geographies, with deeper roots and brand in Indonesia, but behind Grab on profitability, and fintech depth. What matters for this thesis isn't who has more users, it's what the rivalry does to margins. Southeast Asian on-demand has been an incentive war, and the clearest single driver of Grab's margin improvement is that incentive spend fell from about 20% of GMV in 2019 to roughly 7.6% by 2023 as the field consolidated and Grab pulled ahead. Whether that keeps improving is the real question.

Grab–GoTo merger looks like a possibility in 2026: combined, the two would hold roughly 80% of the region's ride and food delivery business, which would effectively end the incentive war and directly improve Grab’s margin. However, the “no-merger” path is still defensible, Grab's ~$5.0B net cash and a loan book heading past $2B by year end let it outspend any regional peer on incentives while building a lending and payments business the pure ride hailers can't replicate.

Sea is a different kind of threat: strong in e-commerce and growing in consumer finance, but with no ride-hailing or on demand delivery, so Grab's mobility position is at no risk but the finance risk where the two overlap — GrabPay holds ~38% of the wallet market in Malaysia and ~35% in Singapore.

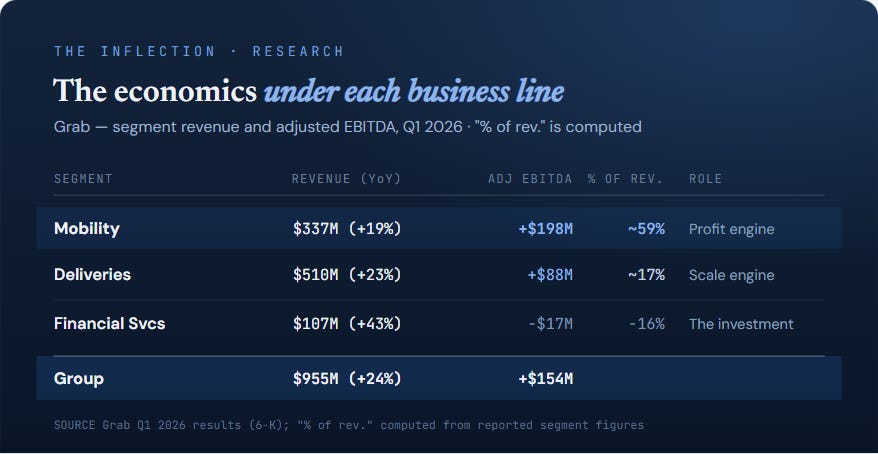

Regarding how much each business generates, here is what each engine actually earned in Q1'26.

Mobility is the profit engine: Grab’s Mobility “revenue” is essentially the commission, that is $337M of revenue contributing to $198M of segment adjusted EBITDA, but roughly 59% of its own revenue.

Deliveries is the scale engine, still thin: The largest revenue line $510M of revenue contributed $88M of segment adjusted EBITDA.

GrabFin is the line being funded: $107M of revenue at a −$17M segment loss.

Chart 4. The economics under each business line. Mobility is the high-margin engine, Deliveries is the thin, scaling line; GrabFin is the funded investment. Segment revenue and EBITDA are reported; “% of revenue” is computed. Source: Grab Q1 2026 results (6-K).

Cross-sell only matters if the profitable lines can fund the unprofitable one, so the funding goes: Mobility and Deliveries together generate about $286M of segment profit a quarter; that covers GrabFin's −$17M drag and roughly $115M of regional corporate cost, and still leaves $154M of group adjusted EBITDA.

Deliveries is a low-margin business, but Mobility is high-margin business, for comparison against Uber, Grab 8.9%-of-GMV margin sits above Uber's blended ~4.6%-of-bookings group margin. The cash building GrabFin's $1.4B loan book isn't borrowed against the future, it's taken by the ride business today. Grab doesn't break out per-line margins beyond segment EBITDA, so the "% of revenue" column below is computed from the reported segment figures.

The Real Inflection: Is GrabFin’s Turnaround What Rerates the Stock?

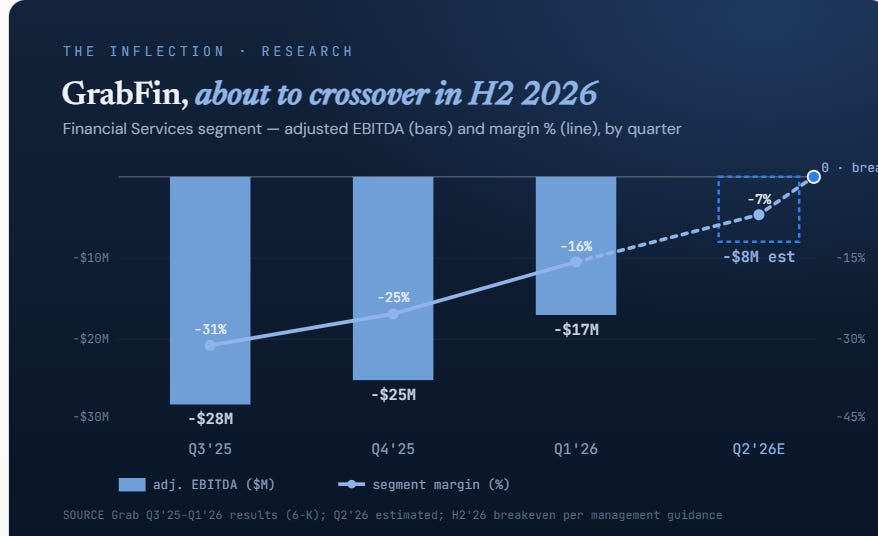

GrabFin is still loss making, but it’s about to crossover in H2 2026 according to management. In Q1’26 the segment’s adjusted-EBITDA loss narrowed to −$17M from −$30M a year earlier — a margin of −15.7% of revenue, up from −41.1% in the prior-year quarter, a 25 point improvement in twelve months.

Chart 4 · GrabFin about to turn profitable. The segment loss has narrowed every quarter — −$28M → −$25M → −$17M — with the margin improving from −31% to −16% of revenue as the loan book seasons. Management guides breakeven in H2 2026; my Q2'26 estimate (dashed) is −$8M / ~−7%. Source: Grab Q3'25–Q1'26 results (6-K); Q2'26 estimated.

Here's why that crossover matters, in Q1'26 the segment's −$17M loss is what holds group adjusted EBITDA at $154M and a 16.2% margin; strip GrabFin out and the rest of Grab already runs near roughly 18% margin. So the flip does two things at once

First it removes the drag worth about $68M annualized at today's run-rate, roughly 1.7 points of group margin.

Second, past breakeven GrabFin turns from subtractor to contributor: on ~$430M of annualized revenue (growing 40%+) and a loan book heading from $1.44B to $2B, even a mid-teens segment margin is ~+$60M a year. The crossover is worth $150–200M+ of group EBITDA, which a meaningful slice of the ~$1B of growth the $1.5B 2028 target needs. That's why I think GrabFin is the single biggest lever to the EBITDA target.

CFO Peter Oey reiterated that GrabFin is on track to reach EBITDA breakeven in the second half of 2026.

The honest risk is the loan book provision upfront, the same one MercadoLibre and Klarna are experiencing, and part of why both trade cheap right now. When Grab writes a loan it books the expected credit loss immediately, at origination, while the interest income arrives over the following months. Grow the book 130% and you pile provisions today against revenue that shows up later, so each cohort looks unprofitable the day it's written and turns profitable as it seasons. GrabFin's blended book looks stressed only because the new cohorts outweigh the seasoned ones, the same reason MELI's margin compressed even as its fintech revenue re-accelerated past 50%. It's also why the loss is narrowing narrowing (−$28M → −$17M over two quarters) while the loan book doubles: the seasoned cohorts are starting to win.

The pattern I'm leaning on is one Nubank makes explicit: as a cohort ages it monetizes more and more. Nubank's blended ARPAC sits near $12 a month, but customers 4+ years on the platform generate $25–27 — the mature cohorts are worth double. Grab own cohort’s disclosure shows GMV per user climbing to ~1.4x by year two, ~1.9x by year three, and ~3.6x by year five, indexed to each cohort's first year (2016 cohort).

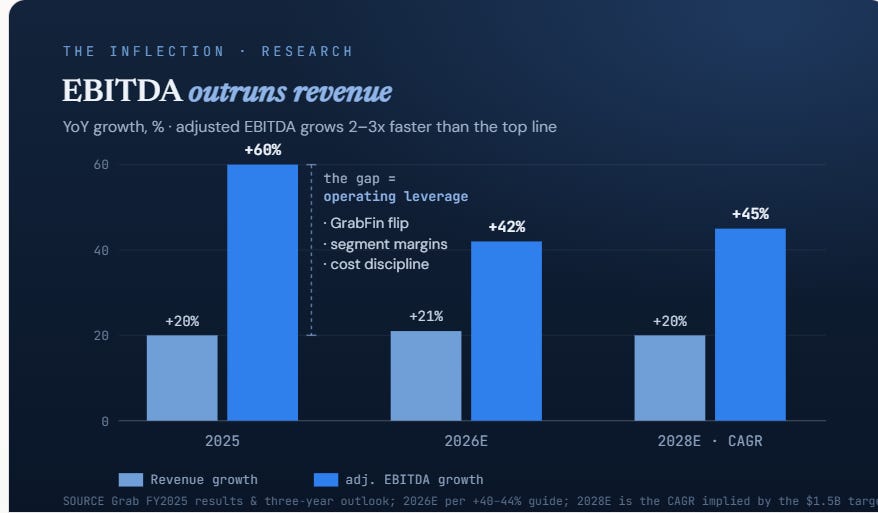

GrabFin flipping is the single biggest lever contributing to Adjusted EBITDA but it isn’t the only one. Getting adjusted EBITDA from $500M to $1.5B by 2028, a triple on a top line growing only ~20% a year, takes three levers working together.

Alongside GrabFin’s flip: corporate cost discipline: SG&A fell from 116% of revenue in 2021 to 24.5% in 2025, and R&D from 52.7% to 12.7% per the Q4’25 commentary.

and segment margins still climbing toward their targets: Mobility around 8.9% of GMV, Deliveries at 2.3% against a 4%+ goal.

Chart 5 · EBITDA outruns revenue. Adjusted EBITDA grows 40–60% a year against a 20% revenue growth, the gap is operating leverage, from GrabFin's flip, climbing segment margins, and cost discipline. 2025 is actual; 2026E is the +40–44% guide; 2028E is the CAGR implied by the $1.5B adjusted-EBITDA target.

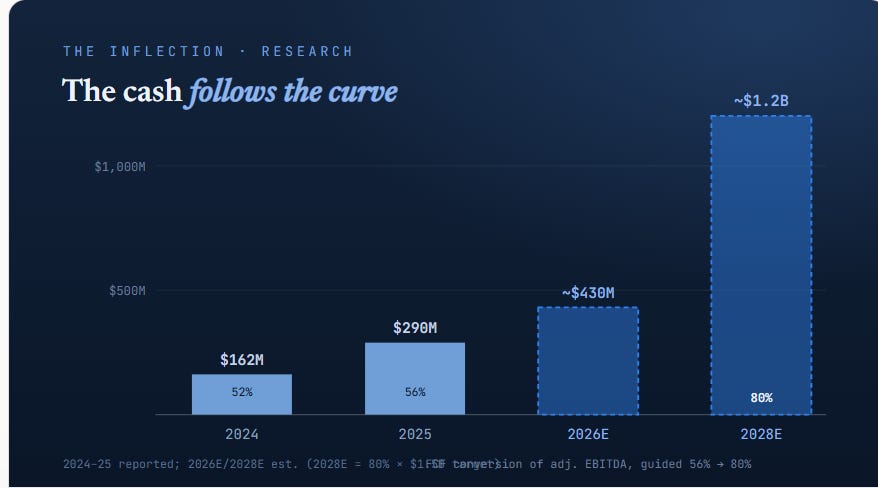

The cash follows the same shape. Adjusted FCF went from $162M (2024) to $290M (2025), and management guides FCF conversion from 56% toward 80% by 2028 — which on the $1.5B EBITDA target is more than $1.2B of free cash flow.

Chart 6. FCF grows. Adjusted free cash flow: $162M in 2024, $290M in 2025, then estimated as EBITDA scales and management's guided conversion rises from 56% toward 80%. The 2028E bar (~$1.2B) is 80% of the $1.5B EBITDA target.

That’s the pattern on Grab, EBITDA and cash growth faster than revenue. Revenue growths 20% a year while adjusted EBITDA grows 40–60% and that gap is exactly the margin expansion from cost discipline, climbing segment margins, and the GrabFin flip.

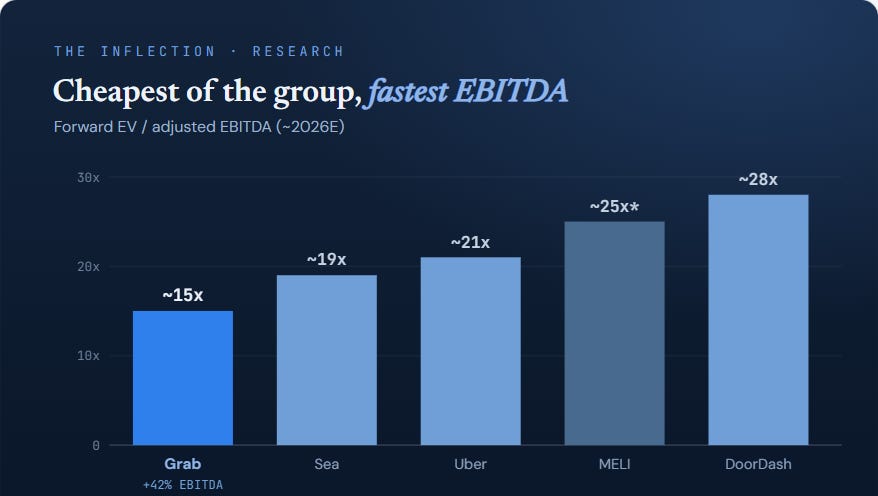

Cheaper Than Sea, Uber, MELI and DoorDash — and Growing EBITDA Faster

Why EV/EBITDA and not P/E? Because GRAB’s entire plan is stated in adjusted EBITDA and free cash flow. So I value Grab the way it’s actually run — on a cash-and-EBITDA basis — and check that against peers.

At the latets closing price $3.90, Grab is about $16.0B of market cap, but around $5.0B of that is net cash, close to a third of the company. Strip the cash and the operating business trades near ~15x forward (2026E) adjusted EBITDA, against

Sea at ~19x

Uber at ~21x

MELI at ~25x

DoorDash at ~28x

Grab is the cheapest of the group while growing EBITDA the fastest (~42% guided). Sea is the closest regional comparison but has no mobility; Uber the closest model in different markets; DoorDash is the pure delivery comparison.

Chart 7. Valuation against peers. On forward EV/adjusted EBITDA, Grab is the cheapest of its multi-line peers while growing EBITDA ~42% faster than any of them.

So at this price what you’re actually buying? Rather than a DCF model, the FCF is still early and growing fast, so discounting it would dress up guesses as intrinsic value, I’ll use the same framework we previously used for MELI, a credible path to roughly 20% growth a year for five years. From $3.90, that means about $9.70 by 2031. The three things have to hold for the case

Revenue compounds ~20%. Grab grew revenue 20% in 2025 and 24% in Q1’26; ~20% over five years is continued execution as growth normalizes.

EBITDA scales far faster than operating leverage. Adjusted EBITDA triples from $500M (2025) to $1.5B (2028) on the company’s own guide, the GrabFin flip, climbing segment margins, and cost discipline and keeps compounding after contributing to higher-margins and higher FCF.

No re-rating needed. At today’s ~15x EV/EBITDA, extend the EBITDA plan at ~20% past 2028 and you reach ~$2.5B by 2031; at 15x plus the ~$5B net cash growing, that’s roughly $10 a share, about 21% a year from $3.90.

And the three scenarios:

Bear $3.20 (-18% in <12 months). GrabFin breakeven slips past H2'26, growth stalls near 17-18% with no rerate, the multiple compresses toward ~11x forward EBITDA, back near the 52-week low. The ~$1.22/share net cash floor is why this is −18% and not a lower.

Base $5.90 (+51% in 12-24 months). GrabFin breaks even on schedule, EBITDA tracks toward $1.5B, FCF conversion ramps toward 80%, and the multiple holds or re rates modestly.

Bull $7.90 (+92% in 2028). The GoTo merger clears and ends the price war, the foodpanda Taiwan and Stash acquisiton accrete on top of guidance, and the multiple expands toward Uber’s ~21x on a larger EBITDA base.

Chart 8 · The setup three scenarios. Bear, base and bull from the $3.90 close (July 2, 2026

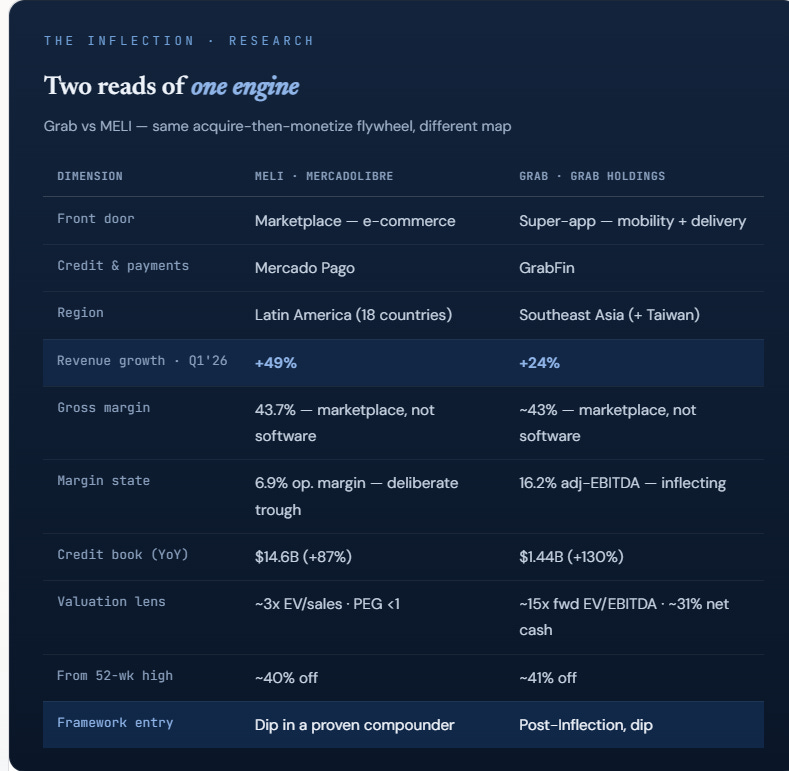

Equivara Portfolio: The Case for Grab and MELI

MELI is a marketplace with a credit and payments engine (Mercado Pago). GRAB is a transaction super-app (mobility + delivery) with a credit-and-payments engine (GrabFin).

So why is a consumer platform worth adding at all? Because it repeats the one engine I've watched compound, the NU/SoFi/Robinhood/Crowdstrike/Klarn shape of acquire cheap then monetize in regions I don't own, and it's available right now at the two entries my framework is built for. MELI is ~40% off their highs (dips in proven compounders); Grab is post first profit with its next inflection, GrabFin's breakeven still ahead. The flywheel is the part I want repeated, because I've seen it work; the map is the new part.

There's a gross margin checklist too. The software portfolio companies wants >80% gross margin, a rule that fits CrowdStrike, Palantir, Rubrik and Cloudflare and none of these consumer-platform apps. Grab and MELI all run gross margins >40%, because they carry real logistics, delivery and credit-loss costs. The right lens for a platform isn't software gross margin; it's operating leverage and EBITDA-margin expansion plus take rate economics, which is exactly why this whole Grab dive is built on the EBITDA line, not the gross margin line. I'm adapting the checklist for the sector.

To be clear about what this is, the Equivara Portfolio dont own neither today, and it isn’t a buy call on either, it’s a framework note on how they’d fit.

Disclosure: I do not own GRAB or MELI. Positions: NU, SOFI, HOOD, PLTR, CRWD, RBRK, NET, CHYM, KLAR, QXO. This is my personal investment thesis, not investment advice — I am not a registered investment or financial adviser, and nothing here is a recommendation to buy or sell any security. Do your own research and size positions to your own risk tolerance.

Sources & basis: Figures are drawn from primary filings, Grab’s Q4 2025 and Q1 2026 results (6-K) and earnings-call commentary, plus the most recent quarterly results of the holdings and comparison names cited (8-Ks / 6-Ks / press releases). Current-price, market-cap and net-cash figures are as of the July 2, 2026 close and will move.

Great article. Since Uber is one of my highest-conviction picks right now - do you see any disruption risk for Grab in the SEA-market? As far as I know is Uber still holding a big position in Grab...

Good breakdown. One nitpick it reads like it's hedging every claim instead of committing to a view. "Cheapest in the group" especially.... that's often the tell that a stock deserves its discount not a hidden bargain.